When you live in a place that’s prone to violent storms–tornadoes, high winds, and hail–odds are, at some point, your house will fall victim to damage. Hail damage, in particular, is one of the most common insurance claims filed each year, and in a best-case scenario, can lead to your insurer paying for a brand-new roof. But how do you know that they’ll have your back when you need them? We don’t want you to throw a Hail Mary (pun intended), so let’s discuss.

Choosing Between RCV and ACV Insurance Plans

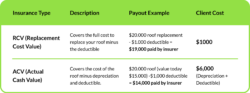

The first variable to look at is the type of homeowners insurance you have. In a nutshell, they’re either Replacement Cost Value (RCV) or Actual Cash Value (ACV) plans. The former carries a more expensive premium cost, but if your roof is damaged, they’ll pay for the full cost of a replacement for a similar quality roof (minus your deductible). With an ACV policy, on the other hand, they factor in depreciation and will only pay you for the value of your roof in today’s dollars. It’s tempting to save your pennies with a cheaper ACV policy, but you may be on the hook for tens of thousands of dollars when you need a new roof. So, go with RCV if you can.

Filing Insurance Claims Post-Storm

The next factor is the date of loss (DOL), which is simply the date the storm occurred. Most insurance companies allow you to file a claim for up to one year from that date. After that, you’re on your own. Both the date of loss and the type of plan you have are non-negotiables with insurance companies, so it’s important to have the appropriate coverage and to file a claim in a timely manner.

Assuming you do both of those things, the next obvious variable is the actual extent of the damage. A tree falling on your roof or a tornado tearing a section off will be hard for an insurer to ignore, but a wind storm or hail storm can be a gray area. Generally speaking, they need to see roughly eight to 10 identifiable hail hits in a 10-foot by 10-foot square (we call it a square) on any face of the roof for a hail claim. But what if they only find six? What if hail pellets were small, but the storm lasted for hours? There can be significant weakening of your shingles, but the evidence of hail is in the form of tiny granules that rubbed off. This can be harder to prove.

How Insurance Companies Handle Storm Damage Claims

Your insurance company has an obligation to serve you, their client, in a faithful and timely manner. But let’s face it, they don’t make billions in profit each year by paying every valid claim that comes their way. Most of the time, if your roof is indeed in need of replacement, they will give you the new roof you deserve. For the times they don’t, it’s important to partner with a reputable roofing company that can advocate for you on your behalf.

Why Partner with Brody Allen Exteriors?

With Brody Allen by your side, your odds of filing a successful claim go up drastically. We’ll make sure they perform a proper inspection and, if need be, push for a re-inspection. We’ll negotiate with them to ensure they provide you with a quality roof and that they pay for every penny beyond your deductible. We’ll take on the stressful parts so that all you have to do is choose the colors you like. After all, we don’t make any money unless your new roof is paid for in full and you’re happy with it. Contact us today.